And just like that 2022 has come to an end. This past year will prove to be memorable for the rapid changes in the market, the ongoing uncertainty we find ourselves living in and our continued search for a ‘new norm’.

Let’s now shift our focus to 2023 and how we can make it the best year ever. Despite the predicted retractions and continued headwinds we face, accomplishing even the loftiest of goals is possible if you take the time to go through proper goal-setting actions. There are countless articles and videos on how to set goals and methods to track them. Here are a couple of articles to help you define your goals and establish methods to crush them! Whatever your goals are, we wish you luck in accomplishing them this year.

We would like to wish everyone a Merry Christmas and a Happy New Year!

Our office will be closed Friday, December 23rd, and Monday, December 26th through Friday, December 30th. Our reps and staff will be available via email and phone.

Brian Finkelmeyer is the senior director of new-vehicle solutions at Cox Automotive.

My daughter and I love staring contests. Our rules are the same as everyone’s—whoever blinks first loses.

Lately, I’ve sensed a similar staring contest emerging in the new car business between consumers, dealers, and automakers. The question is who will blink first?

Before 2020, when dealership lots were overflowing with new-vehicle inventory, manufacturers were always quick to blink—offering bigger and better incentives to entice shoppers. Total industry incentive spend was estimated to be between $50-$60 billion per year. When holiday bonus cash and $179 lease offers didn’t move enough metal, the OEMs would blink again. They had Enterprise and Hertz on speed dial to unload excess inventory.

Back then, the automakers incentivized their dealers to blink with stair-step, volume-based sales programs. Consumers learned the best way to win a good deal on a new car was to keep staring until the last day of the month. Dealers would always blink when there was a $50,000 bonus check riding on the next unit sold.

But the microchip crisis changed all that. With demand far exceeding supply, average transaction prices have increased roughly $10,000 since COVID, hitting $48,681 last month. With incentives at rock bottom, it appears many consumers have just closed their eyes entirely as they signed contracts for new-vehicle purchases, with an average payment of $762 a month. The days of waiting until the last day of the month have turned into waiting 60 days to receive your pre-ordered new car.

After a two-year drought, dealer lots are starting to fill back up. Inventory levels are now up 77% compared to November 2021. Days’ supply has also climbed from 29 to 53. So, with inventory beginning to build and talk of an economic recession looming, the car companies must be ready to blink, right?

Nope: The car companies are staring straight ahead with no expression on their face.

The average incentive spend in November 2021 was $1,896 versus this November at $1,066. That’s a 43% DECREASE in incentives year over year. Many dealers have begun sounding the alarm of softening demand and the necessity for automakers to bring back better incentives. One dealer recently commented, “The sell ‘til the lot is empty party is over!”

But these same anxious dealers continue to post record new-car grosses in the $5,000-$6,000 range, including F&I. With grosses that strong, the OEMs are in no rush to bring back incentives—they’re waiting for dealers to blink first.

Why are the manufacturers feeling so confident? My sense is that their confidence comes from consumers, the very ones who continue to buy new vehicles absent any significant incentives. New-vehicle sales in November were up 10.8% versus the prior year; luxury sales as a percentage of the total industry continue to grow, hitting 18.2% of the market in November. With continued strong grosses and growing retail sales, the OEMs are in no mood to blink.

But here’s the hard truth. It’s highly unlikely that the industry can get back to the glory days of annual sales in the 16-to-17 million range when the average retail price is north of $48,000. For sales volume to grow, the average selling price will need to come down to expand the pool of potential buyers. Automakers and dealers should take note that Walmart recently outperformed analysts’ expectations in their grocery business, as more affluent shoppers steered away from traditional grocery stores to hedge against higher prices and inflation.

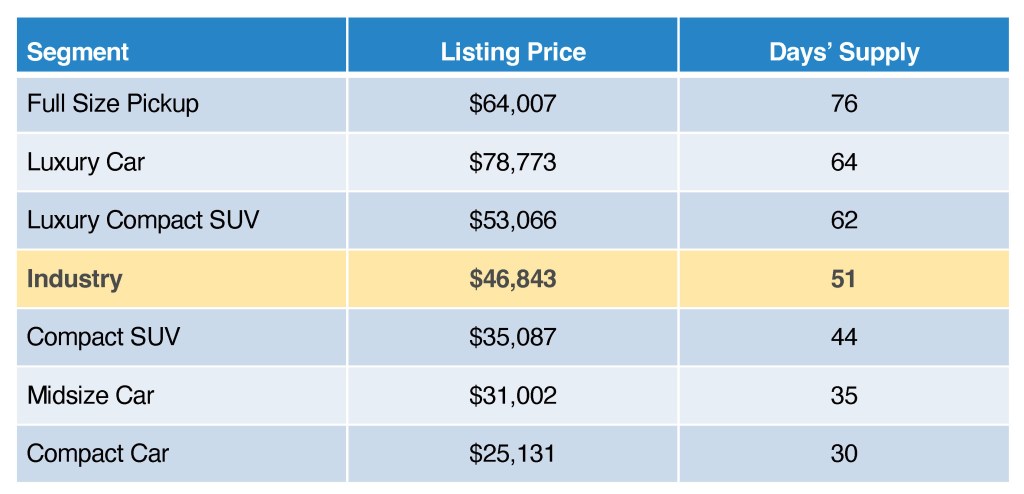

Not surprisingly, there are clear signs of softening demand for more expensive segments with rising days of supply, while affordable inventory segments remain tight. A quick look at the chart below shows that supplies are most constrained for $35,000 and below vehicles in compact SUVs, midsize and compact car segments.

NOVEMBER NEW-VEHICLE INVENTORY ESTIMATES

Given all this, I’m curious to see who will blink first in 2023. Will the automakers blink and begin doling out richer incentives or a more affordable mix? Or will dealers blink, facing rising floorplan costs and decide it’s in their best interest to step back from selling almost every new vehicle at MSRP or above?

I’m not sure how this will all play out in the year ahead, but one thing is true: Until the consumer shows a willingness to blink, the automakers and dealers will be more formidable than my daughter at the staring contest.

The article was written by Brian Finkelmeyer the senior director of new-vehicle solutions at Cox Automotive and was originally published by Cox Automotive.

About 65% of Ford dealers have agreed to sell electric vehicles as the company invests billions to expand production and sales of the battery-powered cars and trucks, CEO Jim Farley said Monday.

Ford offered its dealers the option to become “EV-certified” under one of two programs — with investments of $500,000 or $1.2 million.

Ford, unlike crosstown rival General Motors, is allowing dealers to opt out of selling EVs and continue to sell the company’s cars.

DETROIT – About 65% of Ford Motor’s dealers have agreed to sell electric vehicles as the company invests billions to expand production and sales of the battery-powered cars and trucks, CEO Jim Farley said Monday.

About 1,920 of Ford’s nearly 3,000 dealers in the U.S. agreed to sell EVs, according to Farley. He said roughly 80% of those dealers opted for the higher level of investment for EVs.

Ford offered its dealers the option to become “EV-certified” under one of two programs — with expected investments of $500,000 or $1.2 million. Dealers in the higher tier, which carries upfront costs of $900,000, receive “elite” certification and be allocated more EVs.

Ford, unlike crosstown rival General Motors, is allowing dealers to opt out of selling EVs and continue to sell the company’s cars. GM has offered buyouts to Buick and Cadillac dealers that don’t want to invest to sell EVs.

Dealers who decided not to invest in EVs may do so when Ford reopens the certification process in 2027.

“We think that the EV adoption in the U.S. will take time, so we wanted to give dealers a chance to come back,” Farley said during an Automotive News conference.

Ford’s plans to sell EVs have been a point of contention since the company split off its all-electric vehicle business earlier this year into a separate division known as Model e. Farley said the automaker and its dealers needed to lower costs, increase profits and deliver better, more consistent customer sales experiences.

Farley on Monday also reiterated that a direct-sales model is estimated to be thousands of dollars cheaper for the automaker than the auto industry’s traditional franchised system.

Wall Street analysts have largely viewed direct-to-consumer sales as a benefit to optimize profit. However, there have been growing pains for Tesla, which uses the sales model, when it comes to servicing its vehicles.

Ford’s current lineup of all-electric vehicles includes the Ford F-150 Lightning pickup, Mustang Mach-E crossover and e-Transit van. The automaker is expected to release a litany of other EVs globally under a plan to invest tens of billion of dollars in the technologies by 2026.

The latest reading of the consumer price index showed that used cars are one of the few categories with prices that have fallen from a year earlier.

However, the large runup in prices before that means consumers are still paying 33% more for used cars than they would if normal depreciation had occurred, according to car-shopping app CoPilot.

Electric vehicle prices, which jumped earlier in the year when gas prices were climbing, are now down 20% from their peak in July.

In the latest inflation reading, used cars are one of the few categories with prices that are lower than they were a year ago.

While the consumer price index — which measures price changes for a variety of consumer goods and services — was up 7.1% in November from a year earlier, used cars and truck prices posted an annual 3.3% decline. That compares to some categories that have kept climbing far above year-ago prices, such as eggs (49.1%) and airfare (36%). New car prices are 7.2% higher.

Despite sliding prices for used vehicles, they remain 33% higher than where they’d be if normal depreciation were occurring, said Pat Ryan, founder and CEO of CoPilot, a car-shopping app.

“It’s important to remember that prices are still grossly inflated compared to all normal market conditions,” Ryan said.

“In the new year, we can expect more substantial and accelerated price drops across the board, as vehicle inventory continues to replenish,” said Ryan, adding that dealers also are responding to consumers’ growing resistance to paying record-high car prices.

Demand in the used car market skyrocketed during the pandemic as supply-chain issues hampered automakers’ ability to produce new vehicles. However, the situation is easing slowly with modest improvements in inventory on dealer lots as rising interest rates put pressure on affordability.

Price drops vary among car types and age

While used-car prices are easing from their highs, the decreases depend at least partly on their age and the type of vehicle.

Used electric vehicles have seen the largest drop: The average price of $54,314 in early December is down 20% from a record high of $75,324 in July, according to CoPilot data.

For used hybrids, the average price of $43,574 is a 12% drop from the peak of $49,809 in July. For both segments, whose demand rose earlier in the year when gas prices were headed higher, an easing in gas prices also coincided with a decrease in demand for EVs and hybrids.

Among body types, SUVs and minivans have seen the largest drop this year. List prices for used SUVs average $41,468, down 7% from a peak of $44,824 in March. Used minivans are averaging $24,992, down 8% from $27,257 in March.

By age, 1- to 3-year-old cars come with an average price of $38,987, down 8% from a peak of $42,375 in July.

Among those 4 to 7 years old, the average price is $27,137, a 13% drop from the peak of $31,265 in January. And in the 8-to-13-year-old bracket, the average price of $16,601 is also down 13% from a high of $19,215 in April.

While prices are expected to continue sliding next year, some buyers may not want to wait.

“If you can pay cash now and avoid skyrocketing interest rates [on loans], this month is the best time to buy in over a year,” Ryan said. “With prices finally down year-over-year … and dealers eager to hit year-end sales targets, it could be a good time to negotiate.”

For most buyers, however, “our advice is to wait for the used-car market to finally return closer to normal levels in 2023,” Ryan said.

On the heels of giving many thanks and taking stock on all we are thankful for over this past Thanksgiving weekend; we begin to look forward to arguably the most magical time of the year.

December is typically a robust month for our industries, and this year is setting up to deliver another strong finish. Dealers are seeing a bit more inventory, used car pricing has somewhat settled into a comfortable position, and the recent rise in interest rates hasn’t seemed to slow sales as much as some anticipated. Dealers should consider these headwinds in their 2023 planning and forecasting.

Here are a few items which seem to be picking up energy in our recent conversations with dealers across the country.

After announcing massive investment requirements for its dealers, Ford delays decision date to December 2nd.

As the team at ADS looks back on 2022 and the many successes we’ve had, we are proud to have the partnerships we have with so many dealers and industry leading providers. Without the resolute support of so many, we wouldn’t be able to be so focused on exceeding our dealer’s goals and objectives.

Financial institutions covered by the Safeguards Rule must comply with certain provisions by June 9, 2023

The Federal Trade Commission today announced it is extending by six months the deadline for companies to comply with some of the changes the agency implemented to strengthen the data security safeguards financial institutions must put in place to protect their customers’ personal information. The deadline for complying with some of the updated requirements of the Safeguards Rule is now June 9, 2023.

The Safeguards Rule requires non-banking financial institutions, such as mortgage brokers, motor vehicle dealers, and payday lenders, to develop, implement, and maintain a comprehensive security program to keep their customers’ information safe.

The Commission is extending the deadline based on reports, including a letter from the Small Business Administration’s Office of Advocacy, that there is a shortage of qualified personnel to implement information security programs and that supply chain issues may lead to delays in obtaining necessary equipment for upgrading security systems. These difficulties were exacerbated by the COVID-19 pandemic. These issues may make it difficult for financial institutions, especially small ones, to come into compliance by the deadline.

The FTC approved changes to the Safeguards Rule in October 2021 that include more specific criteria for what safeguards financial institutions must implement as part of their information security programs. While many provisions of the rule went into effect 30 days after publication of the rule in the Federal Register, other sections of the rule were set to go into effect on December 9, 2022. The provisions of the updated rule specifically affected by the six-month extension include requirements that covered financial institutions:

designate a qualified individual to oversee their information security program,

develop a written risk assessment,

limit and monitor who can access sensitive customer information,

encrypt all sensitive information,

train security personnel,

develop an incident response plan,

periodically assess the security practices of service providers, and

implement multi-factor authentication or another method with equivalent protection for any individual accessing customer information.

The Commission vote to extend the deadline was 4-0. Commissioner Wilson issued a separate statement.

Dealers will get an extra month to decide whether to spend up to $1.2M on chargers and other upgrades the automaker is requiring for certification to sell EVs after 2023.

DETROIT — Ford Motor Co. is giving its dealers an extra month to decide whether they will agree to invest up to $1.2 million and follow other new standards the automaker is imposing so they can sell electric vehicles after next year.

The Oct. 31 deadline has been pushed back to Dec. 2 after some retailers asked for more time to make a decision, according to Ford spokesman Marty Gunsberg.

“We value our relationship with our dealers and have decided to provide additional time for dealers who have not yet decided or asked for more time,” Gunsberg said in a statement.

He declined to say how many dealers have already opted in, saying Ford will provide figures after the enrollment period ends.

The new deadline more closely aligns with the Dec. 15 deadline Lincoln dealers face for a similar program requiring up to $900 million in investment. Dealers who sell both brands would have to invest in each program.

The Ford standards are divided into two tiers with different investment levels in fast chargers and staff training. Dealers who choose the lower dollar amount will be limited in the number of EVs they can sell.

Dealers who don’t make the upgrades will be limited to selling internal-combustion vehicles and hybrids from the Ford brand.

The EV sales cap has rankled some state dealer associations, who argue that it violates state laws. The Virginia Automobile Dealers Association earlier this month sent a letter to Ford CEO Jim Farley and other executives asking them to reconsider the program and revise the rules.

Separately, a group of automotive trade association executives, representing associations in Virginia and 11 other southern states, this week asked Ford to “reconsider the Ford Model e program as it is currently described,” saying it “includes unreasonable restrictions on dealer autonomy.” Model e is the name of the EV division that Farley created this year and oversees as its president.

The new sales standards require dealers to set nonnegotiable prices for EVs. Those who choose the lower-priced certification tier won’t be allowed to carry any EVs in inventory, with their customers having to order exactly what they want for later delivery.

Ford has said each of its roughly 3,000 U.S. dealers can choose whether to opt in to the standards, and it will not force any to do so.

Dealers who opt in will be certified to sell EVs from Jan. 1, 2024, until the end of 2026. Those who don’t will have another opportunity to be certified for EV sales starting in 2027, but again, won’t be required to do so to retain their franchise, officials have said.

(Bloomberg) — AutoNation Inc., the biggest US chain of car dealerships, warned that used-vehicle prices are softening as rising interest rates curb demand from more price-sensitive buyers.

The company said Thursday that third-quarter earnings rose to $6 a share excluding some items. That was below the $6.29 a share average of analysts’ estimates. Revenue increased 4% to $6.67 billion, roughly in line with the average of Wall Street projections.

Mike Manley, who took over as chief executive officer of AutoNation a year ago, said he’s been aggressively turning over his portfolio of used cars to make sure he doesn’t get stuck selling them for less than he paid.

“We’re beginning to see used-car prices mitigate with faster depreciation” among mainstream and budget cars, Manley said in an interview. “We benefit from the mix of our portfolio being premium luxury.”

Shares of the company, which also said its board approved a stock buyback of up to $1 billion, pared an early gain of as much as 6.7% to trade up 3.2% to $105.64 as of 9:57 a.m. in New York.

Separately, Hertz Global Holdings Inc. said Thursday that its depreciation costs jumped in the third quarter, reflecting the decline in prices its used cars fetch at auction. Still, the rental-car company narrowly beat Wall Street’s estimates for profit in the period.

Pent-Up Demand

AutoNation’s CEO said new-vehicle inventory is still tight, despite the chip shortage beginning to ease, and there is strong, pent-up demand for vehicles priced above $30,000.

“It’s easing rather than becoming a glut,” he said.

New-car inventory will remain below pre-pandemic levels next year as automakers try to preserve margins to pay for electrification, Manley said on an earnings call Thursday.

In the used-car market, it’s just a matter of time before weaker prices at car auctions filter through to the retail market, pressuring margins for dealers, he said.

Last month, used-car retailer CarMax Inc. said profit from wholesale vehicles dropped 30% in its second quarter as buyers encountered “affordability challenges” and its bank of used cars depreciated.

In the post-pandemic climate of inventory shortages and heightened consumer demand, industry analysts predicted automakers would sell as many vehicles as they could build. But now, just as supply chains and inventories are starting to flow again, there are new pressures on the horizon. Inflation, and the interest rate hikes meant to ease it, are leading to higher auto financing costs and cooling demand for new cars, according to Agent Entrepreneur.

Last month, the average interest rate on a new vehicle purchase hit 5.7%, an increase from about 4% in 2021. “It seems likely that much of the pent-up demand from limited supply will dissipate quickly as high interest rates erode car buyers’ willingness and ability to buy,” said Cox Automotive Senior Economist Charlie Chesbrough. Adding to the equation, the average price for new vehicles reached $45,971 in Q3 2022, up 10% from a year earlier and the highest of any quarter on record, according to J.D. Power.

The irony for dealerships is that just when new vehicles are finally becoming more available, most car buyers can no longer afford them. AutoPayPlus offers dealerships a solution to this challenge.

AutoPayPlus is an F&I service that uses automated biweekly payments to help car buyers better afford their loan payment, purchase additional products, shorten their trade cycle and return to the dealership with less negative equity. A 10-year analysis has shown that dealerships sell approximately 57% more F&I products on AutoPayPlus deals versus standard retail deals. In addition, results from our company’s top dealer groups reveal a 63% increase in per-vehicle financed income on AutoPayPlus customers.

How does it work? Standard auto loans require one payment every month. Biweekly loan payments divide the monthly amount in half and pay it every two weeks. Because there are 52 weeks in a year, the borrower makes 13 payments over the course of a year (instead of 12) with the extra payment applied to the principal.

These smaller biweekly payments are scheduled to coincide with when the borrower gets paid to make it easier to plan for and ensure timely repayment. On a monthly basis though, the payment amount is the same. Simply put, this biweekly strategy gives dealerships a solution to present affordable payments in challenging times.

A lot has also been written in recent months about the wisdom of generating more revenue from the service department as a way to improve a dealership’s bottom line and, in turn, create customers who return to the dealership to buy their next vehicle. AutoPayPlus can help here, as well.

The company offers dealerships an industry-first fintech solution for increasing profits from customer-pay service and boosting customer retention. AutoPay+PERKS combines the company’s biweekly loan payment service with the added advantage of a Mastercard debit card at no additional cost to the customer or dealer.

Once a customer’s AutoPayPlus account has been active for six months and it’s time for their first service, AutoPayPlus sends them a debit Mastercard co-branded with the dealership’s logo and preloaded with $100 that can only be used at the selling dealership’s service department. A dealer boost program allows dealers to load additional funds to the card, further incentivizing their customers’ return to the dealership. It’s a guaranteed way for dealerships to drive new customers to the service department that doesn’t interfere with any other existing retention program such as pre-paid maintenance and, best of all, it’s easy and can be cost-free for dealerships to implement.

As interest rates increase, car buyers are facing significantly higher auto loan payments. And, with no notable inventory improvements forecasted for the fourth quarter combined with waning new-vehicle demand, Cox Automotive is projecting sales in 2022 will be down more than 9% versus 2021 and at the lowest level in a decade.

Yet, in the face of continued market volatility, supply chain and inventory concerns, and questionable consumer financial strength, opportunity still exists. “The key to a dealership’s success today is to maximize its two primary profit sources,” AutoPayPlus CEO Robert M. Steenbergh explains. “Our programs give agents something to offer their dealerships that no other biweekly program can deliver and a solution to continually build customer loyalty.”