Electric vehicle (EV) sales growth in the U.S. continues to slow, according to sales data analyzed by Kelley Blue Book. In the first quarter of 2024, Americans bought 268,909 new electric vehicles, according to Kelley Blue Book counts. EV share of total new-vehicle sales in Q1 was 7.3%, a decrease from Q4 2023.

While annual EV sales continue to grow in the U.S. market, the growth rate has slowed notably. Sales in Q1 rose 2.6% year over year, but fell 15.2% compared to Q4 2023. The increase last quarter was well below the previous two years.

In Q1 2023, EV sales volumes were up 46.4% year over year and 15.5% quarter over quarter. In Q1 2022, EV sales were higher by 81.2% year over year and 20.4% higher than the previous quarter.

“Electric vehicle sales in the U.S. declined during Q1 2024 – the first quarter-over-quarter downturn since Q2 2020,” said Stephanie Valdez Streaty, director of Industry Insights at Cox Automotive.

“As anticipated, Tesla’s sales took a hit, influencing the overall market dynamics. However, a few brands saw significant EV sales increases, achieving over 50% year-over-year growth. As noted in January, we are calling 2024, ‘the Year of More’. More new products, more incentives, more inventory, more leasing and more infrastructure will drive EV sales higher this year. Even so, we’ll continue to see ups and downs as the industry moves towards electrification.”

Analysts at Cox Automotive had expected a slowdown in EV sales growth. Segment growth typically slows as volume increases. This is certainly true with the market leader Tesla, which reported notably lower global deliveries in Q1 2024.

According to Kelley Blue Book estimates, Tesla sales in the U.S. were down 13.3% year over year – well below the typical double-digit growth that had become routine with the Tesla brand. Tesla’s share of the electric vehicle market in Q1 2024 was 51.3%, down from 61.7% one year earlier.

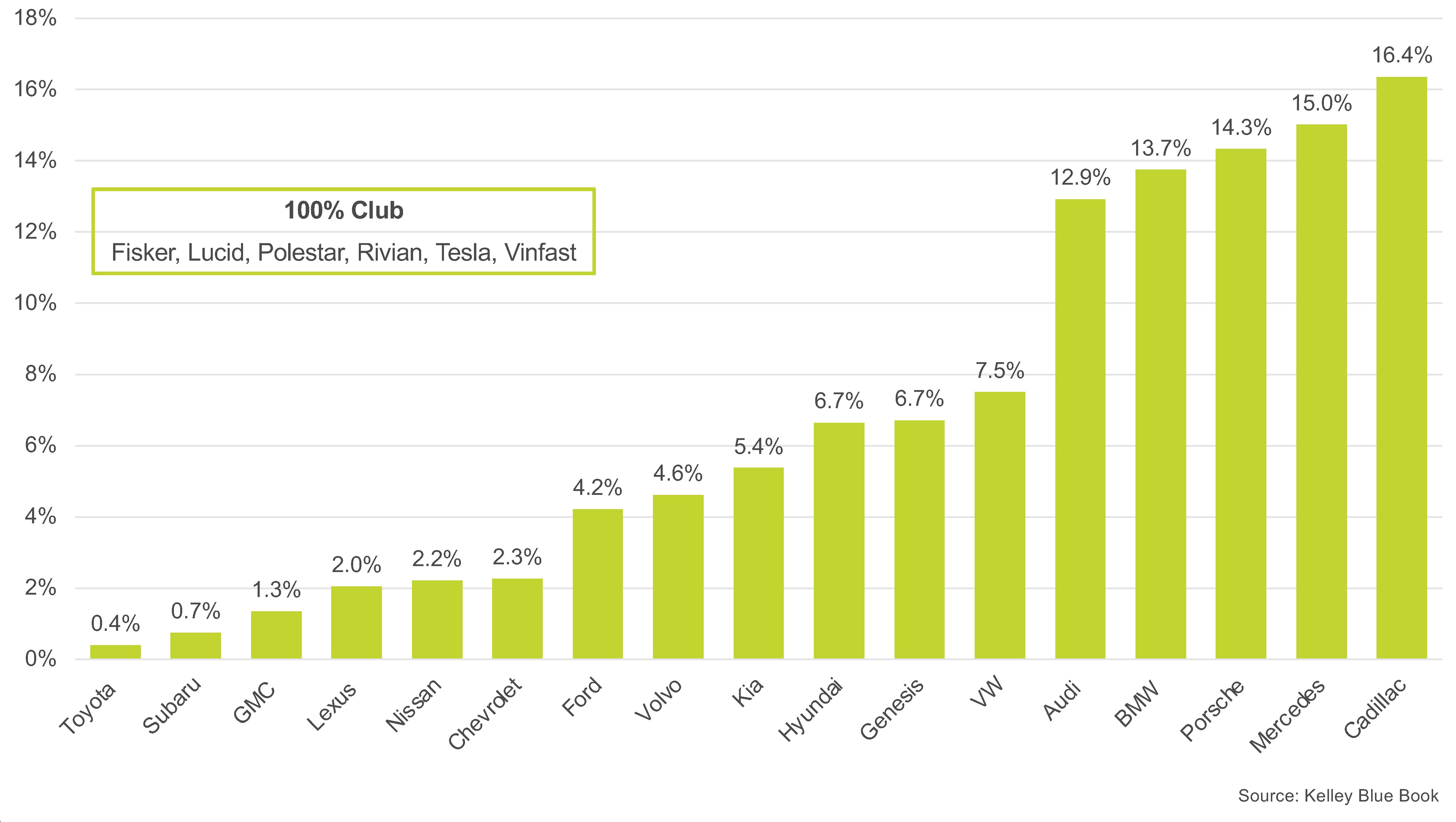

Though the overall year-over-year growth was minimal in Q1, nine manufacturers recorded more than 50% year-over-year growth in EV sales – BMW, Cadillac, Ford, Hyundai, Kia, Lexus, Mercedes, Rivian and Vinfast.

Q1 2024 EV SHARE OF TOTAL BRAND SALES

Notably, lower prices have supported EV sales volume in the U.S., particularly for key Tesla models. The average transaction price for a new EV in Q1 was $55,167, a 9.0% decrease compared to Q1 2023 and down 3.8% quarter over quarter. Tesla’s average transaction price was $52,315 in Q1, down roughly 13.5% year over year. However, lower prices did not generate higher volume.

Many automakers have followed Tesla’s lead and slashed prices. Incentive spending on EVs has increased notably in the past year, another sign of slowing demand. Leasing, too, has increased. In Q1, roughly 27% of all EVs were leased, more than double from the year before. With leasing, many buyers can qualify for the full $7,500 incentive the Inflation Reduction Act offers.

One bright spot in Q1: Strong EV sales from luxury makers, suggesting the EV market continues to be luxury-driven. Cadillac achieved a 499.2% year-over-year increase in electric vehicle sales due to robust sales of its Lyriq model. At Mercedes, EV sales were up 66.9%. BMW posted a 62.6% increase in EV sales compared to Q1 2023. At Audi, Q1 EV sales grew 28.8% year over year.

Meanwhile, sales of the most affordable EV in the U.S. – the Chevy Bolt – have been temporarily halted. Bolt sales fell 64.3% year over year in Q1, hitting just 7,040, as production stopped. A new version of the Bolt is expected to launch in 2025. On the non-luxury side, Ford achieved an 86.1% year-over-year increase in Q1 EV sales with the second-highest EV sales volume behind Tesla.

Cox Automotive forecasts EV sales in the U.S. to increase year over year in 2024, making this year the best year ever for EV sales. Analysts expect EV sales to reach roughly 10% of the market by the end of the year, up from 7.3% in the first quarter.

Trade-in vehicles in negative equity are at a two-year high, according to Edmunds data.

Of those traded in the fourth quarter for new-vehicle purchases, 20.4% were in negative equity, up from about 18% a year earlier and 15% two years earlier, Edmunds says.

The average debt level of borrowers in negative equity situations, meanwhile, climbed from $5,347 in the fourth quarter of 2022 to a record $6,064, which is up 46% from two years earlier.

Edmunds said that with renewed new-vehicle sales due to replenished inventories and the return of incentives, used-vehicle transactions have in turn cooled.

“With demand for near-new vehicles on the decline, used car values are depreciating similarly to the way they did before the pandemic, and negative equity is rearing its ugly head,” said Director of Insights Ivan Drury in a press release.

Consumers who paid more than manufacturer’s suggested retail prices during the pandemic are the most vulnerable to going under water because their newer trade-in models are most prone to big value declines.

The average transaction price of 1-year-old vehicles fell 15% in the quarter to $38,720, Edmunds said. ATP of 2-year-old models fell 9% to $32,583.

It’s the reverse of the pandemic scenario of scarce used vehicles due to supply constraints’ effect on new-vehicle production.

“During the last few years, consumers could jump into new car loans and their trade-ins were shielded from negative equity because some dealers, desperate for used inventory, were willing to pay near original purchase prices,” Drury said. “These days, consumers need to be more careful — especially if they’re trading in newer vehicles — because near-new cars are being hit the hardest by depreciation.”

The RV industry is poised for significant growth in 2024, with wholesale shipments forecasted to reach 350,000 units. This projection comes from the Spring 2024 issue of RV RoadSigns, a quarterly forecast prepared by ITR Economics for the RV Industry Association (RVIA).

“RV shipments are trending in the positive direction and on track for the moderate gains ITR Economics is forecasting in this latest report,” RVIA President & CEO Craig Kirby said in a News & Insights report of the association.

The anticipated range of RV shipments for 2024 is between 334,700 to 365,500 units, centering around a median total of 350,100 units. Such figures suggest an increase of 8.8 to 18.8 percent over the 2023 year-end total of 313,200 units, indicating a robust recovery and expansion within the sector.

“Our data shows a continued desire from consumers to purchase RVs and experience the joys and benefits of the RV lifestyle. We are hopeful that the expected decreases in interest rates and inflation this year will allow more consumers to follow through with their desire to purchase RVs,” Kirby added.

The report identifies several economic indicators that support the optimistic forecast for RV shipments. Notably, housing starts, which historically correlate with RV shipments, are expected to rise in 2024.

Additionally, the expectation of lower interest rates could make RV financing more accessible to potential buyers. The combination of receding inflation and increasing incomes is also expected to create a more conducive environment for the purchase of discretionary items like RVs.

Members of the RV Industry Association have the opportunity to gain further insights into the forecast through a webinar hosted by ITR Economics. Scheduled for Thursday, March 14, at 1 pm Eastern, this webinar aims to provide an in-depth explanation of the forecast, allowing industry stakeholders to better understand the factors driving the anticipated growth.

The RV Industry Association’s efforts to provide detailed insights and forecasts through publications like RV RoadSigns and events such as the upcoming webinar with ITR Economics play a crucial role in supporting the industry’s stakeholders. For more information about the RV Industry Association, click here.

A pair of federal Tax Court decisions at the start of 2024 are painting a concerning picture that the IRS is abusing its authority and attempting to become a quasi-federal governing agency over the insurance industry. The IRS secured a pair of victories against a form of self-insurance for small businesses known as micro-captive insurance. The cases—Keating v. Commissioner and Swift v. Commissioner—used biased fact patterns to support the unfounded principle that all micro-captives are tax shelters or tax schemes.

Neither decision provided guidance nor clarification of how honest micro-captive owners should structure their captive arrangements to remain compliant with IRS regulations. Without such guidance, small to mid-size business owners are subject to open scrutiny at the whim of a federal agency attempting to seize regulatory control of an industry already regulated at the state level.

These victories are contrary to why the 831(b) tax code was written. Similar to what we are seeing today, this code was originally written during a time in which Americans were saddled by a hardened insurance market. Originally passed in the 1980s, Section 831(b) was designed to empower small to mid-sized insurance companies by excluding part of their income from taxation, allowing them to better compete with larger insurance providers and provide a vehicle of self-insurance against risks that may not be covered by insurance companies.

The 2015 Protecting Americans from Tax Hikes Act states that companies are eligible for this type of risk mitigation under Section 831(b) of the tax code when the owner of an insured business holds an interest in the insurer no greater than their interest in the business.

In January, IRS Commissioner Danny Werfel disclosed that nearly 1,100 micro-captives are under IRS investigation. Business owners and plan administrators who are caught up in these audits are then sifted through, with the IRS seeking only cases in which wins are virtually guaranteed. Instead of providing a conclusive determination for other taxpayers who can legitimately benefit from using an 831(b), the IRS uses its ambiguous scrutiny as a deterrent from using these plans, which in some cases can provide a lifeline to small to mid-size businesses.

The IRS has made clear its dislike of micro-captives and is working to eliminate them through its overreach of power and intimidation. This gross misuse by a bureaucratic agency directly contradicts congressional support for the existence of micro-captive insurance. To put it bluntly, the IRS is undermining the laws passed by our nation’s elected representatives and wants to put insurance regulation in the hands of the federal government.

In December, multiple members of the U.S. House Committee on Ways and Means Committee wrote to Werfel to express their disdain about the IRS’s treatment of micro-captives. The members of Congress called for the IRS to work with the insurance industry to develop a mutually agreeable path forward for small to mid-size businesses to utilize this section of the tax code without fear of retribution from the IRS.

The decision in Keating is concerning. In fact, the judge alluded to how the courts believed insurance companies should be regulated.

The McCarran-Ferguson Act of 1945 provides the framework for how the insurance industry is regulated in the U.S.— the federal government can define insurance for federal tax purposes but is prohibited from overreaching into the regulation of insurance, which is instead left to the individual states.

Without action from Congress, or the IRS backing off its assault on our industry, the overreach of power toward micro-captive owners will likely continue, along with its efforts to eventually obtain federal oversight over other parts of the insurance business. The question of overreach by the IRS isn’t a question of if it will stop, but rather a question of when and how. The ripple effects will have far greater implications on the insurance industry as a whole than anything else that may come of this IRS case.

Van Carlson is founder and CEO of SRA 831(b) Admin. He has more than 25 years of experience in the risk management industry and started his career with Farmers Insurance Group.

A Kansas businessman who was indicted Monday on charges connected to altering vehicle odometers is the latest case of odometer fraud in the United States, a crime that costs American car buyers more than $1 billion annually, according to federal authorities.

Adam Newbrey, 31, of Derby, Kansas, was charged with 27 counts of criminal misconduct, including odometer tampering, aggravated identity theft, and mail fraud, among other charges, the U.S. Attorney’s Office for the District of Kansas said in a news release. According to prosecutors, he allegedly purchased used vehicles in Kansas and Oklahoma, and altered the odometers in 2020 and 2021.

Newbrey then used fraudulent documents to obtain vehicle titles from the Kansas Department of Revenue that reflected the falsified odometer readings, prosecutors claim. He is also accused of using the titles with the misrepresented mileage to defraud car buyers.

According to court documents, Newbrey operated three used car dealerships in Wichita: iDeal Motors, Midwest Wholesale, and Prestige Motors. In 2022, iDeal Motors was banned from legally selling cars in Kansas and was fined more than $159,000 following an investigation into consumer complaints about the dealership, KWCH reported.

Odometer fraud across the country is rising each year, according to data firm Carfax. The National Highway Traffic Safety Administration estimates that more than 450,000 vehicles are sold each year with false odometer readings causing consumers to lose over $1 billion annually.

Digital odometers make rollback scams easier

There is a misconception that odometer fraud has declined with digital odometers, according to Carfax research. Recent data suggests that more than 2.1 million vehicles were identified with rolled-back odometers in 2023, a 7% increase from the previous year and up 14% since 2021.

Before modern vehicles, odometers were rolled back manually on a mechanical instrument. But “odometers have since become digital, with the last round of mechanical odometers hitting the road in the early 2000s,” according to Carfax. Now, digital odometers can be rolled-back by removing a car’s circuit board or using equipment that fastens into the vehicle’s electronic circuit.

“Odometer fraud didn’t go away with the introduction of digital odometers,” Patrick Olsen, editor-in-chief at Carfax, said in a statement last December. “We’re still seeing the number of vehicles on the road with a rolled-back odometer rise year-over-year. It takes con artists only a matter of minutes to wipe thousands and thousands of miles off a vehicle’s odometer.”

Typically, higher mileage leads to depreciation in the value of vehicles. Fraudsters tamper with vehicle odometers to rollback the number of miles, deceiving buyers into thinking the car has a lower mileage and a higher purchase price.

As of February, the average used-vehicle listing price was $25,328 — down 4% from a year earlier — according to Cox Automotive. “Though used-vehicle prices are lower now versus 2022 and 2023, they remain much higher than in 2019,” Cox Automotive said in an article.

According to Carfax data, consumers lose an average of $4,000 yearly in rollback scams, which doesn’t include unexpected maintenance and repair costs.

California, Texas, and New York are among states with most rolled-back odometers

Last year, Carfax research found 10 states nationwide with the most cars with rolled-back odometers. Nine of the states saw a rise in rollback scams, while only one remained unchanged:

California: 469,000, up 7.2%

Texas: 277,000, up 12.8%

New York: 100,000, up 9.0%

Florida: 85,400, up 1.4%

Illinois: 79,000, up 7.6%

Pennsylvania: 69,600, up 2.1%

Georgia: 67,600, up 4.0%

Arizona: 57,000, up 4.8%

Virginia: 56,000, unchanged

North Carolina: 49,000, up 8.2%

How to protect yourself from rollback scams

Industry experts say odometer rollback fraud can easily be avoided. Experts recommend examining the vehicle and asking the seller questions about the car’s condition, including the odometer reading.

“If the car shows low mileage but has a lot of wear on the seats, pedals, tires, and steering wheel, that may be a sign that something is amiss,” according to Capital One Auto Navigator.

Capital One and Carfax also recommend the following tips to avoid rollback scams:

Check the car’s history report. Copies can be obtained from websites such as Carfax and AutoCheck.

Review vehicle documents, including the vehicle’s original title, which will show the car’s mileage at the time the title was created. Maintenance and repair records can also show mileage numbers.

Take the car to a mechanic to inspect its condition before buying

Anyone who suspects a seller committed fraud by rolling back the car’s odometer is advised to contact a state enforcement agency. Agencies that investigate odometer rollback cases differ from state to state, according to Carfax.

Welcome to March, everyone! Let’s all hope it comes in and goes out like a lion in terms of sales!

This year’s NADA was fantastic for the ADS leadership team. It was the busiest, most productive, and most enjoyable NADA we can recall. Despite some of the negative outlook for our industries’ sales this year, the overall sentiment was positive, and downright palpable.

We met with many of our valued vendor partners and found time to break some bread with a few of our cherished dealer partners. While in our meetings, we were introduced to several new and exciting programs, and we are excited to roll out to our dealer network in the coming months.

While at NADA we heard dealers talk of ‘cutting back’ on expenses, or ‘trimming the fat’. One of our takeaways from the convention is that there is room to improve on efficiencies and profitability in the stores. When working with the right partners, there are several ways to grow sales, F&I profitability, service retention, and reinsurance results with minimal time investment. Are you ready to investigate a better way of doing business? Give us a call to learn more about how ADS can help you recapture some of those lost profits.

In the next couple of months, the team at ADS will be hard at work putting together and hosting a couple of first-class sales and sales management training classes. Be sure to subscribe to our LinkedIn page as well as our YouTube channel to stay up to date with all things ADS.

Also, ADS has officially entered the risk management business and we are currently providing competitive quotes for dealers on their commercial insurance needs. We are deploying the same truly independent, dealer-first mindset when it comes to preparing the proper package of coverages and premiums. Reach out to your ADS representative to learn more.

As this newsletter is being delivered, the ADS leadership team will be at NADA in Las Vegas. This year’s show is sure to be jammed packed with great meetings, time with some of our valued dealer clients, as well as meeting many new dealers interested in improving their F&I sales process and results.

It was two years ago when NADA was last in Las Vegas. During that show, EV’s were ALL the rage! There was so much talk and hype about EV’s and the demise of the ICE vehicles. It was the FUTURE, or that is what they wanted you to believe.

At that time, we published an article on our skepticism of the prognosticators certainty around the adoption rate of the BEV’s. This was met with some negativity when it came out, but we must remember that two years ago there were months’ worth of backorders for anything electric, so it was only fair to receive some criticism over our cautionary approach.

Now here we are entering another industry event and another manufacturer (Volvo) just pulled back funding on their EV program – much to the pleasure of Wall Street, as their stock surged 20% on the news.

So how did we go from all the rage to a mere footnote in just two years? Is it because the demand was artificial, the talking head CEOs were making statements to appease their investor base, or have we now had two years of real world experience to prove out a lot of the concerns we pointed out. Most likely, it is a combination of all the above.

Let’s be clear, there is a place for EV’s and there is some demand for them, but it is not NEAR what we were being led to believe. The EV market will continue to grow and may even see some significant growth (due to its relatively small market share currently), but the ICE based vehicles that have powered this country for over a century, may just be around for another century…

Richfield, Ohio – Advanced Dealer Solutions is proud to welcome Brandon Kerns as Director of Dealer Services.

Brandon has extensive experience in the automotive business ranging from F&I manager, controller, P&C producer, income development training and working with a floor plan provider.

“Brandon’s experience as a controller will be beneficial to dealers as he works with them to maximize their P&L’s by increasing sales, F&I production and reducing wasteful marketing spend.”– says Bob Mancuso – President of Advanced Dealer Solutions.

“I am excited about being able to provide dealers so many leading programs and services all with an unbiased approach and to have the world-class team at ADS supporting me.” – Brandon Kerns

“Having Brandon and his unique skillset gives our dealers another great resource to utilize as part of doing business with ADS.” – says Ryan Nelson – EVP of Advanced Dealer Solutions. Ryan went on to say, “Brandon’s attention to detail, his understanding of reinsurance and his knowledge of how stores operate, make him an ideal fit for ADS”.

Brandon is based in Denver, CO and will help support the growth of the ADS income development platform throughout the western states.

Advanced Dealer Solutions is a full-service dealer development agency focused on automotive, RV, and powersports dealers across the United States. Please contact 844-320-3722 or info@advdealer.com for any inquiries.

Richfield, Ohio – Advanced Dealer Solutions is proud to welcome Kyle Reese as Managing Partner.

Kyle has nearly 20-years of experience in the automotive industry ranging from working for a large TPA, being a partner in an agency and being a partner in an independent dealership group. His track-record for growth and success is unquestionable.

“Kyle’s experience as a dealer provides him a unique opportunity to help other dealers evaluate their current marketing programs, F&I providers, as well as many other key areas of their business.”– says Bob Mancuso – President of Advanced Dealer Solutions.

“I have known ADS for years and have been impressed with their leadership, professionalism, and vision. I am excited about the opportunity to play a significant role in ADS’s future growth and expansion.” – Kyle Reese

“We are ecstatic to have Kyle as part of the ADS team. His drive, values and purpose fully align with our mission and vision to help dealers achieve more through our independent platform” – says Ryan Nelson – EVP of Advanced Dealer Solutions. Ryan went on to say, “Kyle’s passion for helping dealers succeed is directly in line with ours and makes him a perfect fit for our team”.

Kyle is based in Columbus, OH and will be focused on growing the ADS brand in Central and Southern Ohio as well as Kentucky and Tennessee.

Advanced Dealer Solutions is a full service dealer development agency focused on automotive, RV, and powersports dealers across the United States. Please contact 844-320-3722 or info@advdealer.com for any inquiries.

The data for The 2023 Kerrigan Dealer Survey is based on over 650 responses from franchised auto dealers in Kerrigan Advisors’ proprietary dealer database. Survey responses were collected from June 2023 to October 2023.

2023 Kerrigan Dealer Survey Results Kerrigan Advisors’ fifth annual Dealer Survey was designed to gauge dealer sentiment on the future value of their business, growth plans, earnings expectations, as well as perspectives on franchise values and their trust levels in the OEMs.

The results of this year’s survey found a majority of dealers still have a positive outlook on valuation over the next 12 months with 52% projecting 2023’s strong valuations will sustain into 2024 and 21% expecting an increase next year. That said, more than a quarter of dealers (27%) expect valuations to decrease in the next 12 months, the highest level since the survey’s inception in 2019, and almost double 2019 and 2020’s levels.

The reduction in valuation expectations is consistent with dealers’ views on future profitability (see chart on following page). Only 15% of surveyed dealers project a rise in profits in the next 12 months, while 38% expect a decline. Interestingly, 47% project earnings will stay the same in 2024, a six-percentage point increase from last year and an indication that current earnings, which remain far above pre-pandemic levels, are starting to normalize according to more dealers.

With a rising number of dealers seeing a decline in earnings in the next 12 months, it is not surprising to see an increase in dealers seeking a sale, albeit still a slim minority. 6% of dealers surveyed plan to sell one or more dealerships in the next 12 months, three times 2022’s results. That said, nearly half of dealers still plan to grow their enterprise with 47% looking to add one or more dealerships.

Kerrigan Advisors attributes this growth bias to dealers’ significant capital accounts as a result of more than three years of record profits. Kerrigan Advisors estimates the industry has amassed over $200 billion in pre-tax profits since 2020. In addition to burgeoning capital accounts, the majority of dealers (62%) believe earnings will either stay at 2023’s high level or increase over the next twelve months. This indicates that most dealers do not believe earnings will revert to pre-Covid levels in the near future, if ever, which bodes well for the continuation of a growth bias amongst dealers.

2023 Kerrigan Dealer Survey Results by Franchise

Note: These results reflect the collective view of the 650+ dealers surveyed, regardless of a dealer’s specific franchise ownership.

While the majority of dealers surveyed believe individual franchises will either increase or remain the same in value over the next 12 months, every franchise saw a reduction in the percentage of dealers projecting an increase in value along with a rise in the percentage of dealers expecting a decline in value as compared to 2022. Kerrigan Advisors believes these results are a reflection of the rising discontent within the dealer body regarding OEMs’ electric vehicle (“EV”) strategies and the overabundance of EVs on many dealers’ lots.

Over 40% of surveyed dealers expect these franchises to decline in value in the next 12 months.

Notably, Lincoln and Infiniti’s results are more than double the industry average.

Kerrigan Advisors queried dealers again regarding the expected impact of OEM planned changes to the dealer model on future profitability. The majority of dealers are less concerned than they were in 2022 that OEM changes to retailing will impact their future profitability. Nearly every franchise saw a notable rise in the percentage of dealers who expect no impact on profitability from OEM retailing changes. Kerrigan Advisors believes this marked improvement from the 2022 Dealer Survey is a result of dealers’ skepticism regarding OEMs’ ability to execute on their proposed retailing changes, particularly given weak consumer demand for EVs.

For the first time since Kerrigan Advisors started querying dealers, our firm asked about dealers’ trust level in each franchise. The results were quite noteworthy and echoed the sentiment regarding changes to OEM retailing strategies. Toyota received the top results by far, with 72% of dealers indicating they had a high level of trust in the franchise, over three times higher than the survey average. By contrast, 46% of dealers reported they had no trust in Ford, consistent with the expectation of a decline in future Ford franchise profitability due to the OEM’s EV/future retailing strategy.

Notable Changes for Specific Franchises (2023 versus 2022)

CDJR – CDJR saw a notable increase in dealers expecting the franchise to decline in value, from 24% in 2022 to 53% in 2023 – a 29-percentage point increase. Kerrigan Advisors expects this negative dealer sentiment is a reflection of CDJR’s rising inventory levels and lack of incentive spending. Dealers are concerned Stellantis will continue to oversupply the market with new vehicles resulting in a return to pre-pandemic gross profits on new vehicles and a substantial decline in dealer profitability. Consistent with this change, CDJR ranked 2nd behind Ford as the franchise most expected to see a decline in earnings and value as a result of OEM retailing changes, up from 9th place in last year’s survey. Furthermore, 39% of dealers have no trust in CDJR, placing the OEM as the 4th least trusted franchise.

Ford –Ford remains the franchise most expected to see a decline in profits as a result of the OEM’s changes to its retailing model. Consistent with this negative sentiment, Ford is the non-luxury franchise least expected to see a rise in valuation in the next 12 months. These results reflect dealers’ lack of trust in the OEM with Ford ranking as the least trusted franchise – 48% of dealers surveyed reported that they had no trust in Ford, the highest percentage of any franchise. Kerrigan Advisors expects this negative sentiment to impact Ford’s future blue sky multiple and franchise valuation.

Kia – This franchise surpassed Toyota for the first time in 2022 to become the franchise most expected to increase in value over the next 12 months. Impressively, it sustained its improved results in 2023. Notably, Kia saw one of the largest increases in positive profit expectations as a result of expected changes to its retailing model and ranked as the 8th most trusted franchise. These positive results are consistent with Kerrigan Advisors’ upgrade of Kia’s franchise multiple in the second quarter of 2023 and positive outlook for 2024.

Toyota –Toyota continues to outperform on every level. Most notably, Toyota is the most trusted franchise by dealers, scoring 17 percentage points higher than its nearest non-luxury competitor Subaru. This monumental lead in the trust equation has resulted in the franchise having the highest expected increase in profits as a result of the OEM’s retailing changes with only 7% expecting a decline, the second to lowest level behind its sister franchise, Lexus. Most impressive, despite having the highest blue sky multiple of all non-luxury franchises, dealers expect the franchise’s value will continue to rise. These results are consistent with the buyer demand Kerrigan Advisors sees for Toyota franchises.

The 2023 Kerrigan Dealer Survey results demonstrate the changing auto retail environment and dealers’ perspectives of the OEMs. The majority of dealers project profits and valuations will remain at or rise above post-pandemic levels over the next 12 months, though an increasing minority have a more negative outlook. Nearly half of dealers are seeking to acquire dealerships in the next 12 months, despite higher interest rates, an indication of an overall positive industry outlook. That said, dealers have distinctly varying views on specific franchises, with certain OEMs eliciting a lack of trust and confidence, while others earn a high level of trust and strong profit expectations.

Based on these results, Kerrigan Advisors believes there is more risk to valuations and the buy/sell market going into 2024, though we expect transaction activity will remain elevated as dealers seek to add scale to their business and believe OEM retail changes will have minimal impact on future profits.

Methodology

The data for The Kerrigan Dealer Survey was gathered from Kerrigan Advisors’ annual survey of auto dealers in conjunction with the issuance of The Blue Sky Report. The Kerrigan Dealer Survey is based on 650+ anonymous responses from franchised auto dealers in Kerrigan Advisors’ proprietary dealer database. Responses were collected from June 2023 to October 2023.