As the automotive industry continues to evolve, car dealers are facing a new wave of technological advancements that promise to reshape the landscape. One of the most significant developments is the introduction of robotic salespeople in auto dealerships. While this innovation brings exciting possibilities, it also raises concerns among traditional car dealers about the future of their roles and the overall customer experience. Let’s delve into what this change means for the industry and how dealers can adapt.

The Emergence of Robotic Salespeople

The concept of robotic salespeople is no longer a distant dream. According to a recent article on Motor1.com, dealerships are increasingly adopting robotic salespeople to enhance customer interactions and streamline operations. These robots are designed to provide a seamless and efficient car-buying experience, guiding customers through the process with precision and ease. However, for many dealers, this shift can feel like a threat to their traditional roles and the personal touch they bring to the sales process.

AiMOGA Robot: A Case Study from Malaysia

A prime example of this technological shift is the AiMOGA Robot, which has recently been introduced at the Chery Joystar 4S dealership in Kuala Lumpur, Malaysia. As reported by Chery.my, the AiMOGA Robot is a highly intelligent humanoid developed by Chery and the AiMOGA team. This robot is equipped with advanced multimodal sensing capabilities, allowing it to interpret user commands, physical gestures, and the showroom environment accurately. It can introduce vehicle features, serve beverages, and assist with test drive bookings, all while maintaining a friendly demeanor.

For car dealers, the introduction of such advanced technology can be both exciting and daunting. On one hand, it represents a significant leap forward in customer service and operational efficiency. On the other hand, it raises questions about job security and the future role of human salespeople in the dealership.

Addressing Dealer Concerns

The deployment of robotic salespeople like the AiMOGA Robot is part of a broader strategy to blend technology with a human touch, making every interaction smoother and more connected. However, it’s essential to address the concerns of car dealers who may feel apprehensive about this change.

Job Security: One of the primary concerns for dealers is the potential impact on job security. While robots can handle routine tasks and provide information efficiently, they cannot replace the human element that is crucial in building relationships and trust with customers. Dealers can focus on enhancing their skills in areas where human interaction is irreplaceable, such as personalized customer service, negotiation, and understanding customer needs.

Adapting to Change: Embracing new technology requires a shift in mindset. Dealers can view robotic salespeople as tools that complement their roles rather than replace them. By leveraging the capabilities of robots, dealers can free up time to focus on more complex and value-added tasks, ultimately improving the overall customer experience.

Enhancing Customer Experience: The integration of robotic salespeople can lead to a more efficient and enjoyable car-buying process. Robots can handle repetitive tasks, provide accurate information, and ensure that customers receive consistent service. This allows human salespeople to concentrate on creating meaningful connections and addressing specific customer concerns.

The introduction of robotic salespeople like the AiMOGA Robot marks a significant milestone in the automotive industry. While it brings exciting possibilities for enhancing the car-buying experience, it also presents challenges for traditional car dealers. By embracing this change and focusing on the unique value that human interaction brings, dealers can navigate this transition successfully and continue to thrive in the evolving landscape. Stay tuned to AdvancedDealerSolutions.com for more insights and updates on the latest trends and innovations in the automotive industry.

Electric vehicle (EV) sales growth in the U.S. continues to slow, according to sales data analyzed by Kelley Blue Book. In the first quarter of 2024, Americans bought 268,909 new electric vehicles, according to Kelley Blue Book counts. EV share of total new-vehicle sales in Q1 was 7.3%, a decrease from Q4 2023.

While annual EV sales continue to grow in the U.S. market, the growth rate has slowed notably. Sales in Q1 rose 2.6% year over year, but fell 15.2% compared to Q4 2023. The increase last quarter was well below the previous two years.

In Q1 2023, EV sales volumes were up 46.4% year over year and 15.5% quarter over quarter. In Q1 2022, EV sales were higher by 81.2% year over year and 20.4% higher than the previous quarter.

“Electric vehicle sales in the U.S. declined during Q1 2024 – the first quarter-over-quarter downturn since Q2 2020,” said Stephanie Valdez Streaty, director of Industry Insights at Cox Automotive.

“As anticipated, Tesla’s sales took a hit, influencing the overall market dynamics. However, a few brands saw significant EV sales increases, achieving over 50% year-over-year growth. As noted in January, we are calling 2024, ‘the Year of More’. More new products, more incentives, more inventory, more leasing and more infrastructure will drive EV sales higher this year. Even so, we’ll continue to see ups and downs as the industry moves towards electrification.”

Analysts at Cox Automotive had expected a slowdown in EV sales growth. Segment growth typically slows as volume increases. This is certainly true with the market leader Tesla, which reported notably lower global deliveries in Q1 2024.

According to Kelley Blue Book estimates, Tesla sales in the U.S. were down 13.3% year over year – well below the typical double-digit growth that had become routine with the Tesla brand. Tesla’s share of the electric vehicle market in Q1 2024 was 51.3%, down from 61.7% one year earlier.

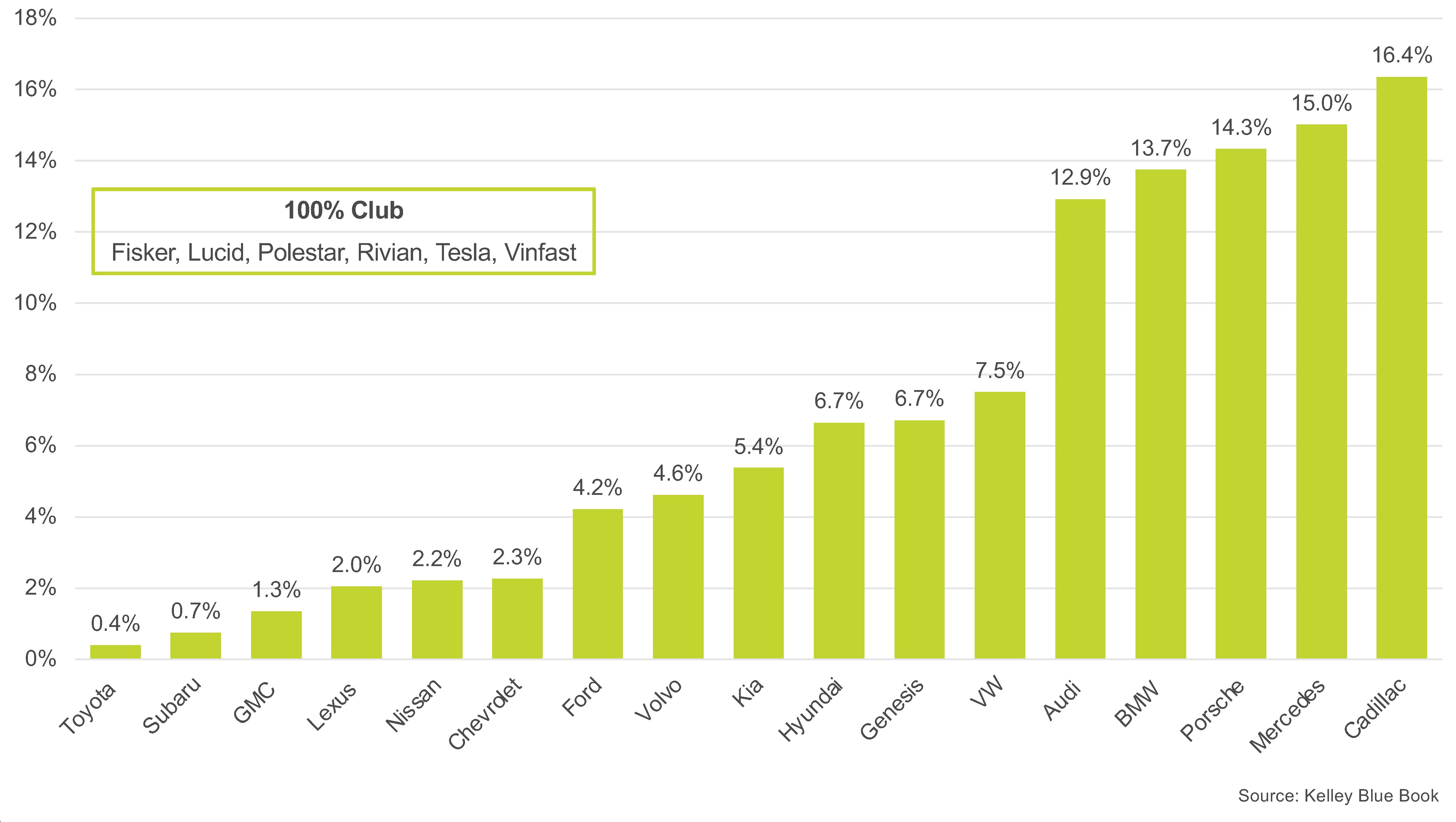

Though the overall year-over-year growth was minimal in Q1, nine manufacturers recorded more than 50% year-over-year growth in EV sales – BMW, Cadillac, Ford, Hyundai, Kia, Lexus, Mercedes, Rivian and Vinfast.

Q1 2024 EV SHARE OF TOTAL BRAND SALES

Notably, lower prices have supported EV sales volume in the U.S., particularly for key Tesla models. The average transaction price for a new EV in Q1 was $55,167, a 9.0% decrease compared to Q1 2023 and down 3.8% quarter over quarter. Tesla’s average transaction price was $52,315 in Q1, down roughly 13.5% year over year. However, lower prices did not generate higher volume.

Many automakers have followed Tesla’s lead and slashed prices. Incentive spending on EVs has increased notably in the past year, another sign of slowing demand. Leasing, too, has increased. In Q1, roughly 27% of all EVs were leased, more than double from the year before. With leasing, many buyers can qualify for the full $7,500 incentive the Inflation Reduction Act offers.

One bright spot in Q1: Strong EV sales from luxury makers, suggesting the EV market continues to be luxury-driven. Cadillac achieved a 499.2% year-over-year increase in electric vehicle sales due to robust sales of its Lyriq model. At Mercedes, EV sales were up 66.9%. BMW posted a 62.6% increase in EV sales compared to Q1 2023. At Audi, Q1 EV sales grew 28.8% year over year.

Meanwhile, sales of the most affordable EV in the U.S. – the Chevy Bolt – have been temporarily halted. Bolt sales fell 64.3% year over year in Q1, hitting just 7,040, as production stopped. A new version of the Bolt is expected to launch in 2025. On the non-luxury side, Ford achieved an 86.1% year-over-year increase in Q1 EV sales with the second-highest EV sales volume behind Tesla.

Cox Automotive forecasts EV sales in the U.S. to increase year over year in 2024, making this year the best year ever for EV sales. Analysts expect EV sales to reach roughly 10% of the market by the end of the year, up from 7.3% in the first quarter.

The U.S. auto industry is entering a “new normal” where automakers and dealers will labor harder to maintain profits, a report by Dave Cantin Group and Kaiser Associates says.

During the COVID-19 pandemic, supplies of vehicles on dealer lots fell. That meant higher vehicle prices and increased margins for automakers and dealers.

That is likely to shift this year, according to the report.

“The U.S. automotive industry has had an exceptional last few years,” the report said. “Indeed over the past 3+ years it seems like everyone won – everyone, that is, except the consumer(who has paid higher prices for fewer choices, longer lead times and more competition to get a vehicle at all.)”

In 2024, industry’s new normal “won’t look quite as attractive as it did in 2023, but better than it did (for manufacturers and dealerships) in 2019,” the report said.

Dave Cantin Group and Kaiser conducted interviews with industry analysts and executives as well as surveying more than 1,000 consumers.

Among the factors cited by the report as having an impact on the industry:

—“The economic climate in the U.S. is healthier than predicted going into 2024 – but a positive macro economic climate increases the complexity facing the industry.”

Interest rates may begin to decline later this year after efforts by the Federal Reserve to curb inflation. In turn, dealers may need to boost inventory and increase advertising spending, according to the report.

“Dealerships should expect to work harder to maintain profitability in 2024,” the report said.

At the same time, declining interest rates “are likely to unlock pent-up demand, resulting in greater vehicle sales.”

—Consumers surveyed are more likely than ever to buy SUVs. Of respondents, 44% said they want an SUV for their next vehicle.

“Consumers may be moving toward SUVs because of reliability, versatility, and safety, despite higher price tags,” the report said. “This shift may also align with brand preference: some of the brands consumers are most likely to buy are primarily known for SUVs.”

Automakers, including General Motors Co., Ford Motor Co., Toyota Motor Corp. and Nissan Motor Co. have retired car models over the past several years. Ford, for example, said in an April 2018 earnings announcement, that 90% of its North American vehicle fleet would be trucks, SUVs and commercial vehicles by 2020.

The report said increased SUV deliveries will mean higher revenues and profits, according to the report.

—International situations such as U.S.-China tensions and Middle East conflicts could still disrupt the industry. “Geopolitical conflicts could drive a U-turn on consumer sentiment” and lower the willingness of automakers “to make strategic investments,” the report said.

U.S. Pours Money Into Chips, but Even Soaring Spending Has Limits

Amid a tech cold war with China, U.S. companies have pledged nearly $200 billion for chip manufacturing projects since early 2020. But the investments are not a silver bullet.

Don Clark reports on the semiconductor industry, and Ana Swanson reports on trade and international economics.

In September, the chip giant Intel gathered officials at a patch of land near Columbus, Ohio, where it pledged to invest at least $20 billion in two new factories to make semiconductors.

A month later, Micron Technology celebrated a new manufacturing site near Syracuse, N.Y., where the chip company expected to spend $20 billion by the end of the decade and eventually perhaps five times that.

And in December, Taiwan Semiconductor Manufacturing Company hosted a shindig in Phoenix, where it plans to triple its investment to $40 billion and build a second new factory to create advanced chips.

The pledges are part of an enormous ramp-up in U.S. chip-making plans over the past 18 months, the scale of which has been likened to Cold War-era investments in the space race. The boom has implications for global technological leadership and geopolitics, with the United States aiming to prevent China from becoming an advanced power in chips, the slices of silicon that have driven the creation of innovative computing devices like smartphones and virtual-reality goggles.

Today, chips are an essential part of modern life even beyond the tech industry’s creations, from military gear and cars to kitchen appliances and toys.

Across the nation, more than 35 companies have pledged nearly $200 billion for manufacturing projects related to chips since the spring of 2020, according to the Semiconductor Industry Association, a trade group. The money is set to be spent in 16 states, including Texas, Arizona and New York on 23 new chip factories, the expansion of nine plants, and investments from companies supplying equipment and materials to the industry.

The push is one facet of an industrial policy initiative by the Biden administration, which is dangling at least $76 billion in grants, tax credits and other subsidies to encourage domestic chip production. Along with providing sweeping funding for infrastructure and clean energy, the efforts constitute the largest U.S. investment in manufacturing arguably since World War II, when the federal government unleashed spending on new ships, pipelines and factories to make aluminum and rubber.

“I’ve never seen a tsunami like this,” said Daniel Armbrust, the former chief executive of Sematech, a now-defunct chip consortium formed in 1987 with the Defense Department and funding from member companies.

President Biden has staked a prominent part of his economic agenda on stimulating U.S. chip production, but his reasons go beyond the economic benefits. Much of the world’s cutting-edge chips today are made in Taiwan, the island to which China claims territorial rights. That has caused fears that semiconductor supply chains may be disrupted in the event of a conflict — and that the United States will be at a technological disadvantage.

The new U.S. production efforts may correct some of these imbalances, industry executives said — but only up to a point.

The new chip factories would take years to build and might not be able to offer the industry’s most advanced manufacturing technology when they begin operations. Companies could also delay or cancel the projects if they aren’t awarded sufficient subsidies by the White House. And a severe shortage in skills may undercut the boom, as the complex factories need many more engineers than the number of students who are graduating from U.S. colleges and universities.

The bonanza of money on U.S. chip production is “not going to try or succeed in accomplishing self-sufficiency,” said Chris Miller, an associate professor of international history at the Fletcher School of Law and Diplomacy at Tufts University, and the author of a recent book on the chip industry’s battles.

White House officials have argued that the chip-making investments will sharply reduce the proportion of chips needed to be purchased from abroad, improving U.S. economic security. At the TSMC event in December, Mr. Biden also highlighted the potential impact on tech companies like Apple that rely on TSMC for their chip-making needs. He said that “it could be a game changer” as more of these companies “bring more of their supply chain home.”

U.S. companies led chip production for decades starting in the late 1950s. But the country’s share of global production capacity gradually slid to around 12 percent from about 37 percent in 1990, as countries in Asia provided incentives to move manufacturing to those shores.

Today, Taiwan accounts for about 22 percent of total chip production and more than 90 percent of the most advanced chips made, according to industry analysts and the Semiconductor Industry Association.

The new spending is set to improve America’s position. A $50 billion government investment is likely to prompt corporate spending that would take the U.S. share of global production to as much as 14 percent by 2030, according to a Boston Consulting Group study in 2020 that was commissioned by the Semiconductor Industry Association.

“It really does put us in the game for the first time in decades,” said John Neuffer, the association’s president, who added that the estimate may be conservative because Congress approved $76 billion in subsidies in a piece of legislation known as the CHIPS Act.

Still, the ramp-up is unlikely to eliminate U.S. dependence on Taiwan for the most advanced chips. Such chips are the most powerful because they pack the highest number of transistors onto each slice of silicon, and they are often held up as a sign of a nation’s technological progress.

Intel long led the race to shrink the size of transistors so more could fit on a chip. That pace of miniaturization is usually described in nanometers, or billionths of a meter, with smaller numbers indicating the most cutting-edge production technology. Then, TSMC surged ahead in recent years.

But at its Phoenix site, TSMC may not import its most advanced manufacturing technology. The company initially announced that it would produce five-nanometer chips at the Phoenix factory, before saying last month that it would also make four-nanometer chips there by 2024 and build a second factory, which will open in 2026, for three-nanometer chips. It stopped short of discussing further advances.

In contrast, TSMC’s factories in Taiwan at the end of 2022 began producing three-nanometer technology. By 2025, factories in Taiwan will probably start supplying Apple with two-nanometer chips, said Handel Jones, chief executive at International Business Strategies.

TSMC and Apple declined to comment.

Whether other chip companies will bring more advanced technology for cutting-edge chips to their new sites is unclear. Samsung Electronics plans to invest $17 billion in a new factory in Texas but has not disclosed its production technology. Intel is manufacturing chips at roughly seven nanometers, though it has said its U.S. factories will turn out three-nanometer chips by 2024 and even more advanced products soon after that.

The spending boom is also set to reduce, though not erase, U.S. reliance on Asia for other kinds of chips. Domestic factories produce only about 4 percent of the world’s memory chips — which are needed to store data in computers, smartphones and other consumer devices — and Micron’s planned investments could eventually raise that percentage.

But there are still likely to be gaps in a catchall variety of older, simpler chips, which were in such short supply over the past two years that U.S. automakers had to shut down factories and produce partly finished vehicles. TSMC is a major producer of some of these chips, but it is focusing its new investments on more profitable plants for advanced chips.

“We still have a dependency that is not being impacted in any way shape or form,” said Michael Hurlston, chief executive of Synaptics, a Silicon Valley chip designer that relies heavily on TSMC’s older factories in Taiwan.

The chip-making boom is expected to create a jobs bonanza of 40,000 new roles in factories and companies that supply them, according to the Semiconductor Industry Association. That would add to about 277,000 U.S. semiconductor industry employees.

But it won’t be easy to fill so many skilled positions. Chip factories typically need technicians to run factory machines and scientists in fields like electrical and chemical engineering. The talent shortage is one of the industry’s toughest challenges, according to recent surveys of executives.

The CHIPS Act contains funding for work force development. The Commerce Department, which is overseeing the doling out of grant money from the CHIPS Act’s funds, has also made it clear that organizations hoping to obtain funding should come up with plans for training and educating workers.

Intel, responding to the issue, plans to invest $100 million to spur training and research at universities, community colleges and other technical educators. Purdue University, which built a new semiconductor laboratory, has set a goal of graduating 1,000 engineers each year and has attracted the chip maker SkyWater Technology to build a $1.8 billion manufacturing plant near its Indiana campus.

Yet training may go only so far, as chip companies compete with other industries that are in dire need of workers.

“We’re going to have to build a semiconductor economy that attracts people when they have a lot of other choices,” Mitch Daniels, who was president of Purdue at the time, said at an event in September.

Since training efforts may take years to bear fruit, industry executives want to make it easier for highly educated foreign workers to obtain visas to work in the United States or stay after they get their degrees. Officials in Washington are aware that comments encouraging more immigration could invite political fire.

But Gina Raimondo, the commerce secretary, was forthright in a speech in November at the Massachusetts Institute of Technology.

Brian Finkelmeyer is the senior director of new-vehicle solutions at Cox Automotive.

My daughter and I love staring contests. Our rules are the same as everyone’s—whoever blinks first loses.

Lately, I’ve sensed a similar staring contest emerging in the new car business between consumers, dealers, and automakers. The question is who will blink first?

Before 2020, when dealership lots were overflowing with new-vehicle inventory, manufacturers were always quick to blink—offering bigger and better incentives to entice shoppers. Total industry incentive spend was estimated to be between $50-$60 billion per year. When holiday bonus cash and $179 lease offers didn’t move enough metal, the OEMs would blink again. They had Enterprise and Hertz on speed dial to unload excess inventory.

Back then, the automakers incentivized their dealers to blink with stair-step, volume-based sales programs. Consumers learned the best way to win a good deal on a new car was to keep staring until the last day of the month. Dealers would always blink when there was a $50,000 bonus check riding on the next unit sold.

But the microchip crisis changed all that. With demand far exceeding supply, average transaction prices have increased roughly $10,000 since COVID, hitting $48,681 last month. With incentives at rock bottom, it appears many consumers have just closed their eyes entirely as they signed contracts for new-vehicle purchases, with an average payment of $762 a month. The days of waiting until the last day of the month have turned into waiting 60 days to receive your pre-ordered new car.

After a two-year drought, dealer lots are starting to fill back up. Inventory levels are now up 77% compared to November 2021. Days’ supply has also climbed from 29 to 53. So, with inventory beginning to build and talk of an economic recession looming, the car companies must be ready to blink, right?

Nope: The car companies are staring straight ahead with no expression on their face.

The average incentive spend in November 2021 was $1,896 versus this November at $1,066. That’s a 43% DECREASE in incentives year over year. Many dealers have begun sounding the alarm of softening demand and the necessity for automakers to bring back better incentives. One dealer recently commented, “The sell ‘til the lot is empty party is over!”

But these same anxious dealers continue to post record new-car grosses in the $5,000-$6,000 range, including F&I. With grosses that strong, the OEMs are in no rush to bring back incentives—they’re waiting for dealers to blink first.

Why are the manufacturers feeling so confident? My sense is that their confidence comes from consumers, the very ones who continue to buy new vehicles absent any significant incentives. New-vehicle sales in November were up 10.8% versus the prior year; luxury sales as a percentage of the total industry continue to grow, hitting 18.2% of the market in November. With continued strong grosses and growing retail sales, the OEMs are in no mood to blink.

But here’s the hard truth. It’s highly unlikely that the industry can get back to the glory days of annual sales in the 16-to-17 million range when the average retail price is north of $48,000. For sales volume to grow, the average selling price will need to come down to expand the pool of potential buyers. Automakers and dealers should take note that Walmart recently outperformed analysts’ expectations in their grocery business, as more affluent shoppers steered away from traditional grocery stores to hedge against higher prices and inflation.

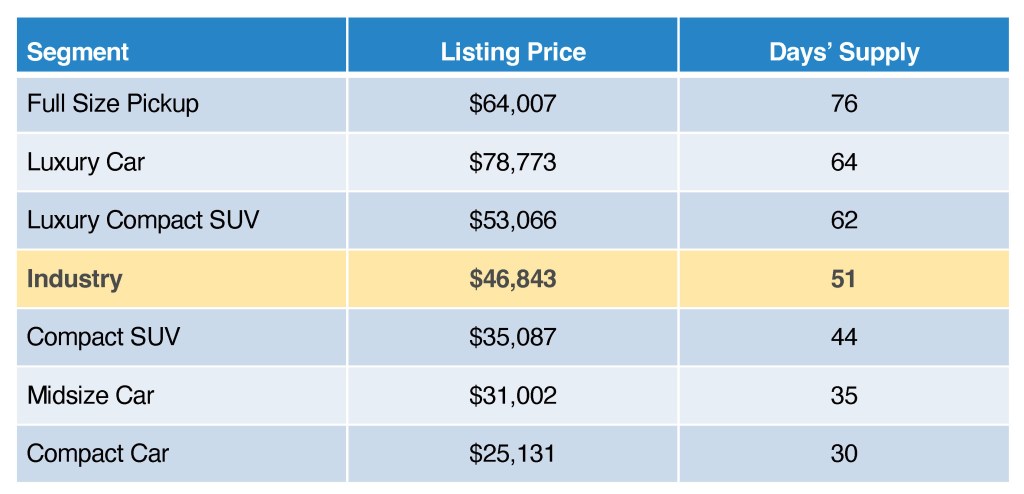

Not surprisingly, there are clear signs of softening demand for more expensive segments with rising days of supply, while affordable inventory segments remain tight. A quick look at the chart below shows that supplies are most constrained for $35,000 and below vehicles in compact SUVs, midsize and compact car segments.

NOVEMBER NEW-VEHICLE INVENTORY ESTIMATES

Given all this, I’m curious to see who will blink first in 2023. Will the automakers blink and begin doling out richer incentives or a more affordable mix? Or will dealers blink, facing rising floorplan costs and decide it’s in their best interest to step back from selling almost every new vehicle at MSRP or above?

I’m not sure how this will all play out in the year ahead, but one thing is true: Until the consumer shows a willingness to blink, the automakers and dealers will be more formidable than my daughter at the staring contest.

The article was written by Brian Finkelmeyer the senior director of new-vehicle solutions at Cox Automotive and was originally published by Cox Automotive.

The current supply issues are creating a unique ‘sellers’ environment for dealers of all types these days and it is unlike any market I have experienced in my 27 years in the retail industry. Whether you are currently selling cars, RVs, or powersports you are seeing customer demand potentially higher than you’ve ever seen and are rightfully enjoying the fruits of scarcity. We all know this is a cycle, and at some point, we will again see rebates, negotiating, and discounts. The fruits dealers are currently harvesting are well deserved after surviving nearly a decade of margin erosion and a continuous sprint to the bottom of the price chain.

I recently attended a couple of industry events and heard story after story about customers agreeing to purchase, and pay top dollar, for their third or even fourth choice of vehicle. On the surface, this seems like an ideal, highly successful model for dealers to live in. While it has been bountiful, I feel there are some adverse effects as well as some missed opportunities worthy of addressing.

There is an old adage, ‘when perceived value exceeds price, you have a sale.’ Right now, the perceived value is the raw availability to conduct a transaction instead of the traditional checklist of wants and needs. Simply having something to sell is all the value a customer needs to see in a retailer. The dealers I know and work with, want more; they want a customer to see value in the transaction, not just being able to conduct a transaction. Of course, dealers want to maximize on the current opportunity, but they also want to perform the balancing act of earning the well-deserved profit, as well as providing long-term value in doing business with their dealership but for years to come.

Assuming dealers are exceeding their customers experience expectations, then we’ll move on to the value of the vehicle. By value, I am not referring to the features and benefits the customer has spent hours online pouring over, but the additional value a dealer can provide by protecting some of the customers risk exposure. Customers often get caught up in the euphoria of the purchase and forget the reality of owning a car, RV or powersport toy. They forget cars get dirty. They forget RV’s get lived in and spills and accidents occur. They forget their side by side could catch the eye of a thief. The risks of these forgotten realities can be mitigated by dealers including protection products on an addendum.

An addendum allows a dealer to enhance the value of a transaction by pre-selecting one or more value-based consumer products and adding them to a ‘Why Buy Here’ of the dealership. These addendums create a unique presentation opportunity for the sales consultant and most likely leads the customer away from a decision based solely on availability, or worse price. Instead of talking about discounts to meet a competitor’s price, the sales consultant can direct the conversation to the benefit of having a vehicle location device with years of monitoring included, as well as the cash benefit to assist in the event of an unrecovered stolen vehicle. Customers will value peace-of-mind over price if they are educated on the benefits before being ‘sold’ the item or being asked to pay a higher price with no explanation of benefits.

There are a few addendums I have seen backfire on dealers. Pinstripes, although spectacular to some, generally don’t command a $1,495 increase to the cost of the vehicle. And believe it or not, there are some that don’t see $999 of value in a set of plastic mudflaps for their Honda Accord. Whereas customers do see value in knowing their vehicle is protected from everyday spills and stains, as well as having some coverage against the environmental effects to today’s modern painted exteriors. Who out there doesn’t relate to a soda, or ketchup packet spilling on their seats or floorboards at some point in their driving history?

The great part about an addendum is it helps clarify the customers value in the vehicle as well as reminding them of the unavoidable perils of owning a vehicle in today’s world. If the customer doesn’t see value, then the addendum can be removed, and you have a sold vehicle at or near MSRP. If the sales consultant properly conveys the value of each item on the addendum, then it is likely the customer will at least purchase one, if not everything the dealer includes on the addendum. Either way, the dealer and customer are in winning situations; value exceeds cost!

A few suggestions:

Make the addendum something of true value to your customers. Leave out frivolous outdated items nobody sees value in. Today’s buyer is too sophisticated and will see through the gimmicks of what is being attempted.

The success of an addendum is directly correlated in the confidence of the presentation by the sales consultant. If the dealership staff doesn’t believe in what is being offered, it will fail and most likely backfire on the dealer.

Disclose anything and everything. Don’t sneak anything in. Proudly display the addendum and additional cost on the vehicle. Give your team the tools to demonstrate the value of each product being offered. Value based protection products sell themselves when explained properly.

Live it. Like most rewarding actions in life, you cannot be passive. You must be active with your value-added items each and every day. Here are a couple ways to keep everyone focused on the value on in the addendum:

Walk around competitions for some additional Saturday spiff money.

Product knowledge quizzes focused on what makes this product so valuable.

Retain the customer. The addendum should have some form of tie back to the selling dealer. Don’t just sell a vehicle, win a lifelong customer. The real gains come from the harnessed lifetime value of a family in the dealership’s community. Believe it or not, people still like doing business with people they know and trust.

About the author: Ryan Nelson has over 25 years of experience in the retail industry and is a Partner at Advanced Dealer Solutions, a leading independent agency specializing in dealership development in the auto, RV and powersports industry.

To learn more about how the right addendum can benefit your dealership, please reach out to Advanced Dealer Solutions at 844-320-3722 or info@advdealer.com