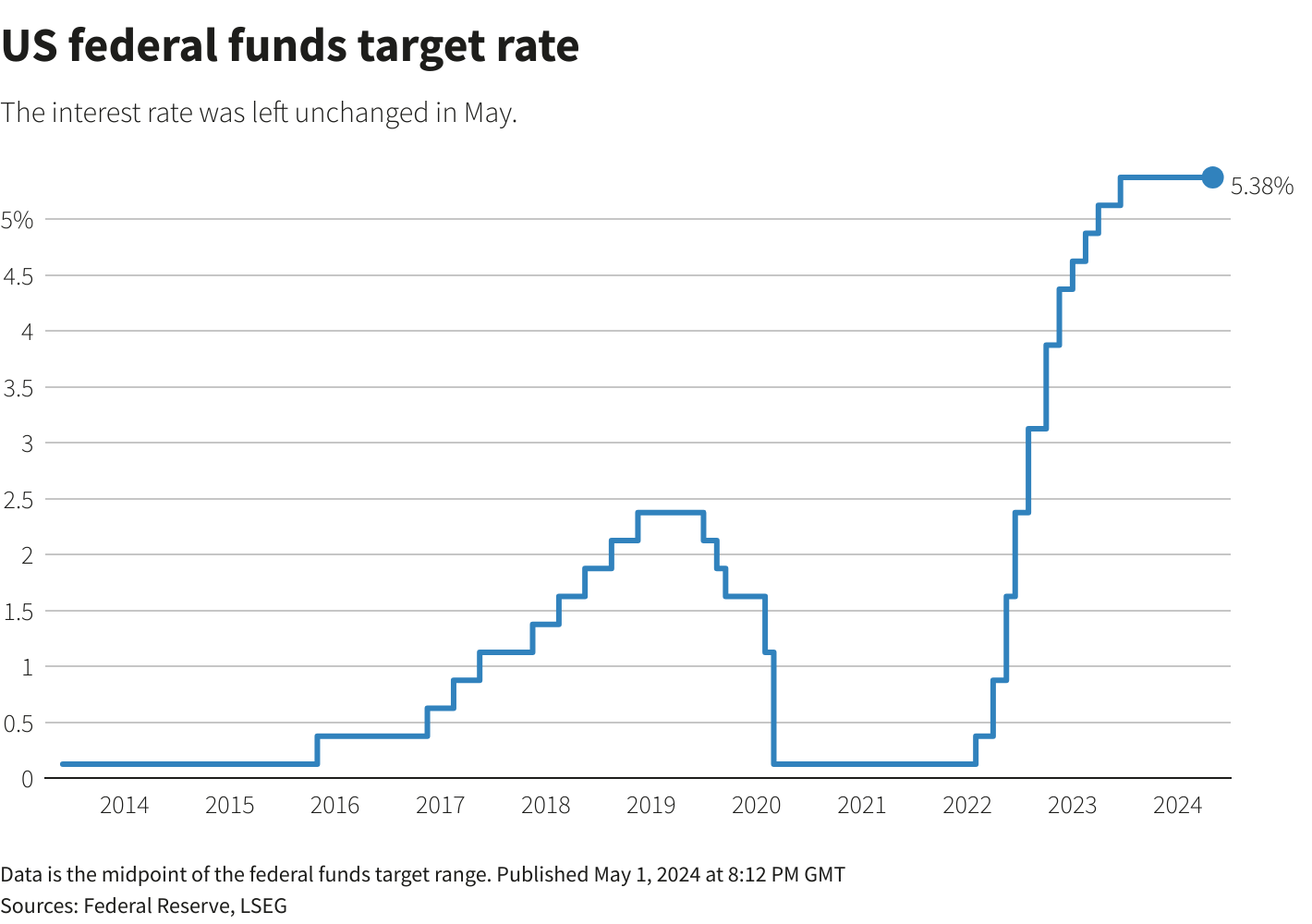

WASHINGTON, May 1 (Reuters) – The U.S. Federal Reserve held interest rates steady on Wednesday and signaled it is still leaning towards eventual reductions in borrowing costs, but put a red flag on recent disappointing inflation readings that could make those rate cuts a while in coming.

Indeed, Fed Chair Jerome Powell said that after starting 2024 with three months of faster-than-expected price increases, it “will take longer than previously expected” for policymakers to become comfortable that inflation will resume the decline towards 2% that had cheered them through much of last year.

That steady progress has stalled for now, and while Powell said rate increases remained unlikely, he set the stage for a potentially extended hold of the benchmark policy rate in the 5.25%-5.50% range that has been in place since July.

U.S. central bankers still believe the current policy rate is putting enough pressure on economic activity to bring inflation under control, Powell said, and they would be content to wait as long as needed for that to become apparent – even if inflation is simply “moving sideways” in the meantime.

The Fed’s preferred inflation measure – the personal consumption expenditures price index – increased at a 2.7% annual rate in March, an acceleration from the prior month.

“Inflation is still too high,” Powell said in a press conference after the end of the Federal Open Market Committee’s two-day policy meeting. “Further progress in bringing it down is not assured and the path forward is uncertain.”

Powell said his forecast remained for inflation to fall over the course of the year, but that “my confidence in that is lower than it was.”

Whether there are rate cuts this year or not remains in doubt.

“If we did have a path where inflation proves more persistent than expected, and where the labor market remains strong but inflation is moving sideways and we’re not gaining greater confidence, well, that would be a case in which it could be appropriate to hold off on rate cuts,” Powell said. “There are paths to not cutting and there are paths to cutting. It’s really going to depend on the data.”

Despite the uncertainty of the current economic moment, Powell’s characterization of rate hikes as “unlikely” cheered investors concerned about a newly hawkish Fed chief.

U.S. stock and bond prices turned higher as Powell preached patience that may delay rate cuts, but also means a high bar for any more hikes. The Fed raised its benchmark policy rate by 5.25 percentage points in 2022 and 2023 to curb a surge in inflation.

Powell’s remarks on Wednesday were “notably less hawkish than many feared,” said analysts at Evercore ISI. “The basic message was that cuts have been delayed, not derailed.”

Investors in contracts tied to the Fed’s policy rate increased bets that rate cuts could begin in September rather than later in the year as reflected in earlier market pricing.

BALANCE SHEET

The Fed’s latest policy statement kept key elements of its economic assessment and policy guidance intact, noting that “inflation has eased” over the past year, and framing its discussion of interest rates around the conditions under which borrowing costs can be lowered.

“The Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably towards 2%,” the Fed repeated in its unanimously-approved statement.

That continues to leave the timing of any rate cut in doubt, and Fed officials made emphatic their concern that the first months of 2024 have done little to help the cause.

“In recent months, there has been a lack of further progress towards the Committee’s 2% inflation objective,” the Fed said in its statement.

The U.S. central bank also announced it will scale back the pace at which it is shrinking its balance sheet starting on June 1, allowing only $25 billion in Treasury bonds to run off each month versus the current $60 billion. Mortgage-backed securities will continue to run off by up to $35 billion monthly.

The step is meant to ensure the financial system does not run short of reserves, as happened in 2019 during the Fed’s last round of “quantitative tightening.”

While the move could loosen financial conditions at the margin at a time when the U.S. central bank is trying to keep pressure on the economy, policymakers insist their balance sheet and interest rate tools serve different ends.

The Fed maintained its overall assessment of economic growth, saying that the economy “continued to expand at a solid pace. Job gains have remained strong and the unemployment rate has remained low.”

Powell reconciled that with the relatively weak, 1.6% growth of gross domestic product in the first quarter by saying that the 3.1% increase in private domestic demand was a better gauge of where the economy stands, with output buttressed by a recent jump in immigration.

Asked about the risk the U.S. was entering a period of “stagflation” with stagnant growth and rising prices, Powell said current conditions are nothing like those seen in the late 1970s when prices were rising more than 10% annually at one point alongside high unemployment.

“Right now we have … pretty solid growth … We have inflation running under 3%,” Powell said. “I don’t see the ‘stag’ and I don’t see the ‘flation.'”

Originally posted by Reuters https://www.reuters.com/markets/rates-bonds/fed-hold-rates-steady-inflation-dims-hopes-policy-easing-2024-05-01/